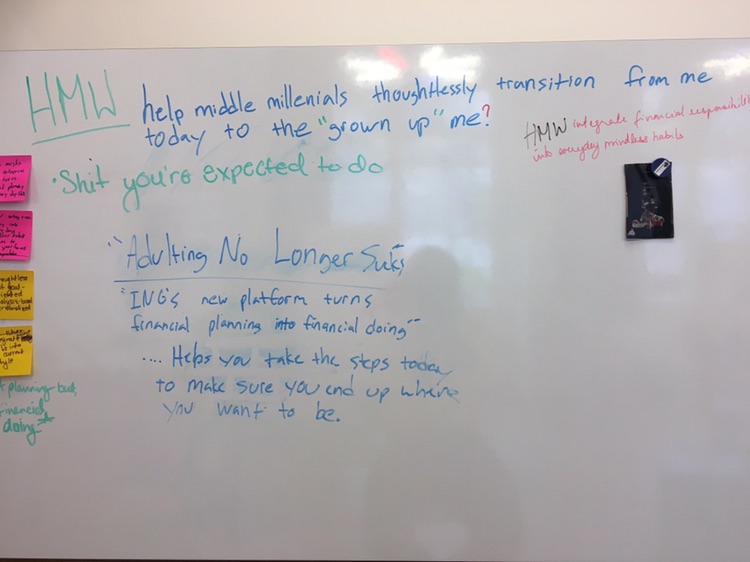

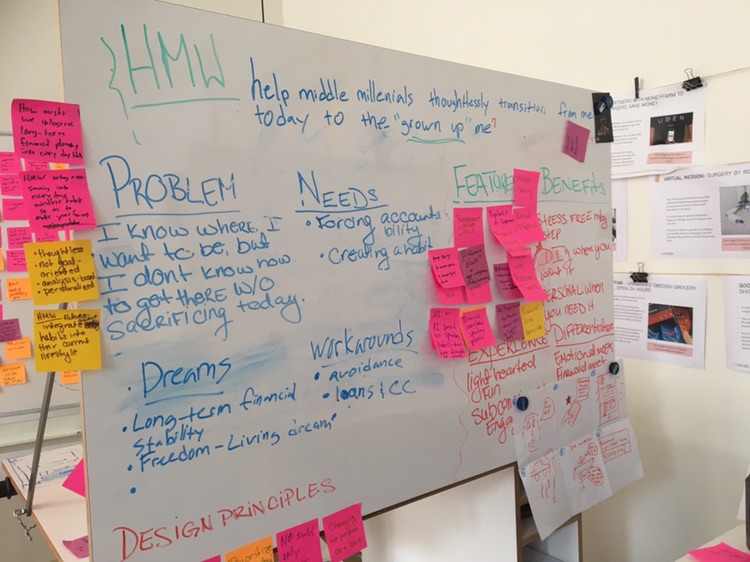

How might we help millennials build good financials habits to transition from “me today” to “grownup me”?

In order to do so, we first needed to understand how people actually build habits. We did deep dive into self-determination theory and other motivation research studies where we found 3 keys to forming lasting habits: Understanding why we do what we do, setting “micro quotas” and “macro goals, and using If-Then behavior chains.

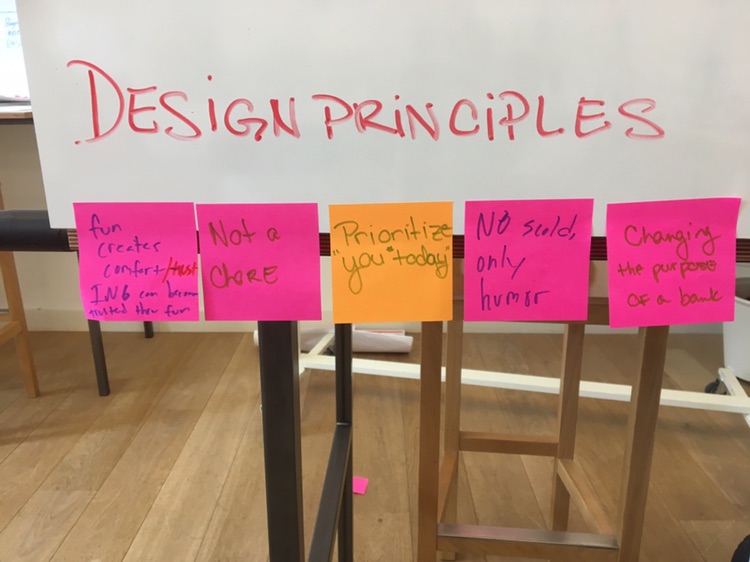

With that perspective and our earlier insights, we established a basic set of design principles. Going forward, whatever solution we landed on had to keep our principles at its core. By confining ourselves to what we've found to be true about this audience, we were able to push our imaginations in the right direction during ideation.

We landed on a service platform that would help younger adults stay engaged with their financial success by first learning how they stay engaged with anything. Starting out with a rough storyboard of how it would work, our team began testing the cohesion and desirability of the proposed solution, making adjustments on the fly in post-interview debriefs.

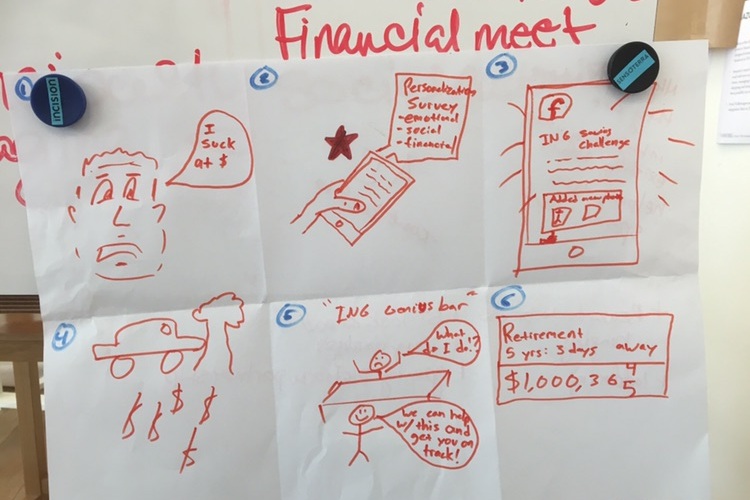

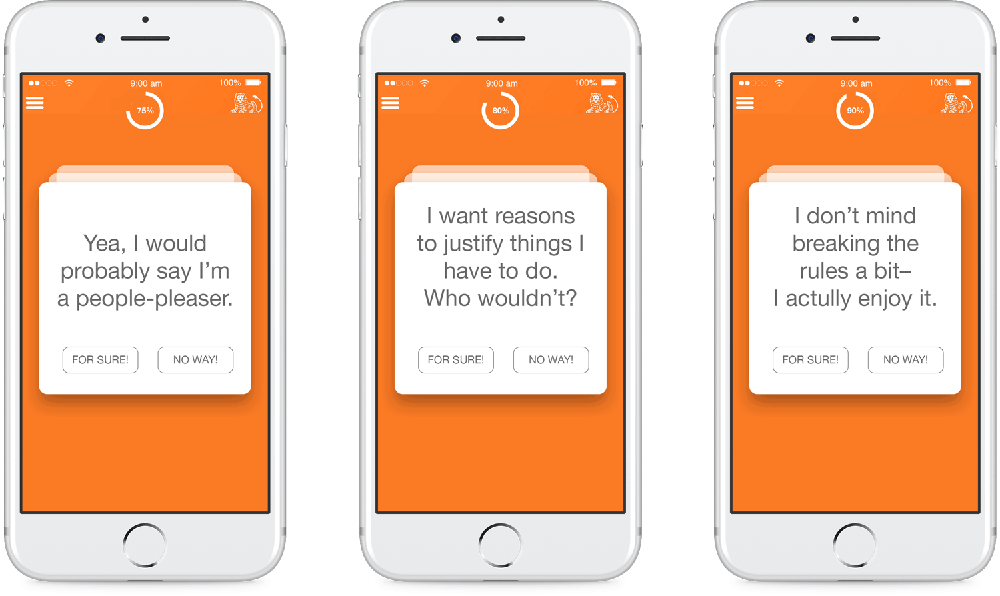

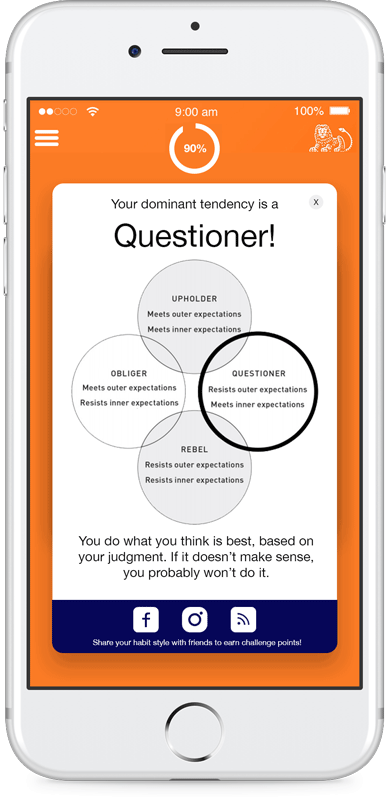

From there, our team prototyped a heuristic mobile game that combines psychographic information with your online social identity and financial data into a profile that shows a user’s individual “habit-forming style.”

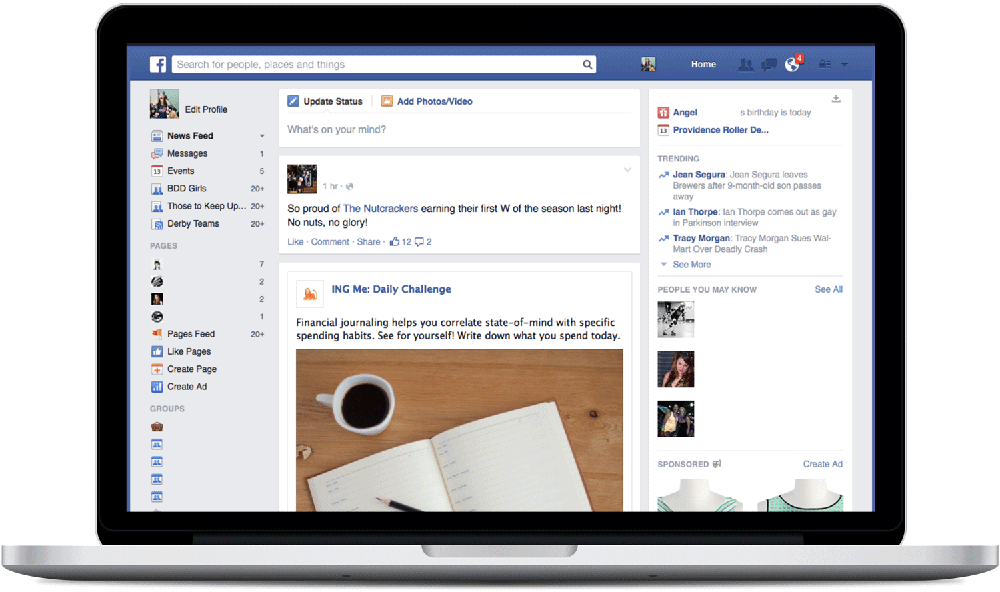

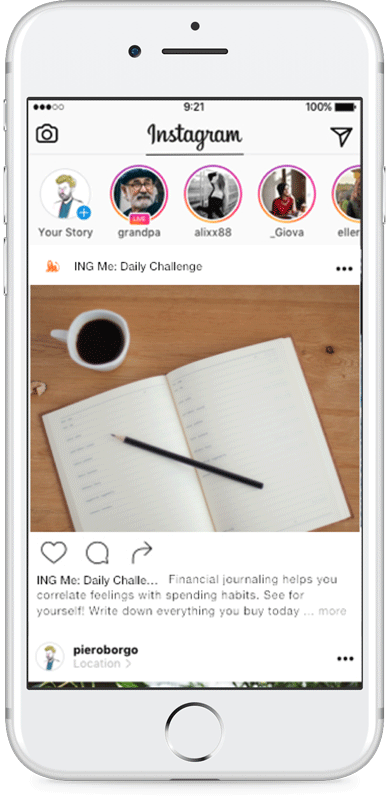

Are you a people-pleaser, willing to take on a task for others, but less willing to take care of yourself? Or maybe you’re a rebel, and you are less likely than others to do as you are told when it comes to adopting a new lifestyle. Whoever you are, that information would be used to pose individualized daily challenges that integrate into the users’ social media feeds, effectively breaking down the macro goal of financial stability into daily micro quotas using if-then behavior chains.

To prevent financial “binges,” the platform integrates surprise rewards into some challenges (Go ahead, girl. Treat yourself).

The platform taps into who you are and what makes you tick, but what about when you slip up? This is an audience who trusts their hairstylist more than their parent’s financial advisor, yet didn’t want to be hassled by either when they weren’t looking for help. We worked around that with a little inspiration from Alcoholics Anonymous. The solution was a casual and comfortable space where you could drop in to see a financial advisor who can help you reset your habit building, no appointment needed. This gave our audience an on-demand shoulder to cry on and a “sponsor” to get back on track.

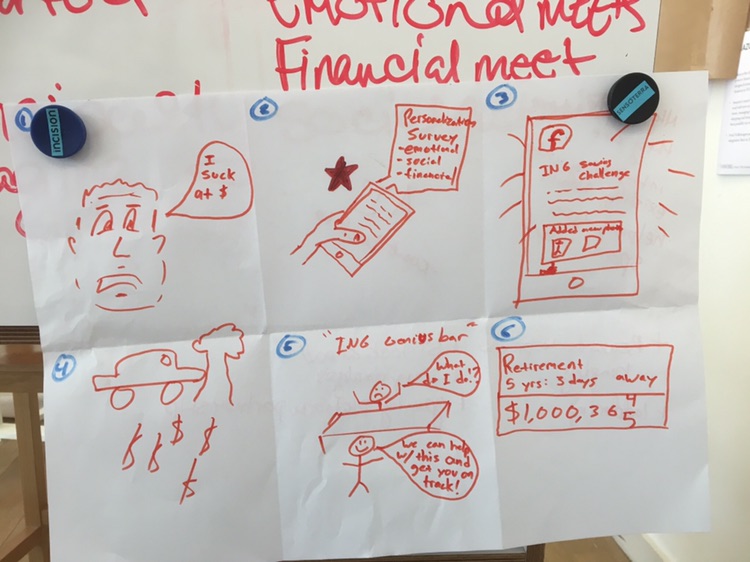

We outlined a set of assumptions for our client to test in the next phases, such as will people visit a flyby financial advisor for quick tips and help? The recommended next step was to create financial advice “Genius Bars” to understand if people would be comfortable enough to talk through their money challenges in passing because, in an ideal world, the future of banking, is the future of personal growth.

foundational research

How might we create a trusted partner for Millennials so as to help them make the right short- and long-term financial decisions?

It’s the question that every major consumer bank is asking itself these days. In an aggressive one-week sprint with a leading international bank, our team set out to find the solution.

We interviewed 20- and 30-somethings from across the board: the self-employed, the family-oriented, the creative types, and so on. When combined with secondary research, these interviews revealed a trending persona among our audience. We called him Vaughn.

Like most millennials, Vaughn values freedom and flexibility, but isn't willing to sacrifice his current lifestyle for long term ‘financial stability.” Unless he has something to save for, like a new car or camera, Vaughn doesn't proactively save.

The funny thing is, even when Vaughn makes arguably poor financial choices, he contends that he knows what to do to be financially secure in the future. For Vaughn, there's a gap in the roadmap toward financial goals. Vaughn knows he'll be okay, but struggles to hold himself accountable in practice. Money management is seen as something he thinks he'll figure out in the long run, but the traditional "grownup" routes to getting there are stressful, restrictive, and dated.

The most meaningful insight from our research was that, without help building sustainable habits, millennials will only save when they have something to save for. The market is rife with brands aiming to solve the problem by facilitating goal-setting Meanwhile, no one is helping them build consistent, sustainable financial habits outside of the one-off occasions. With that perspective, we set out to answer a new question: